Analysis: CIR ruling

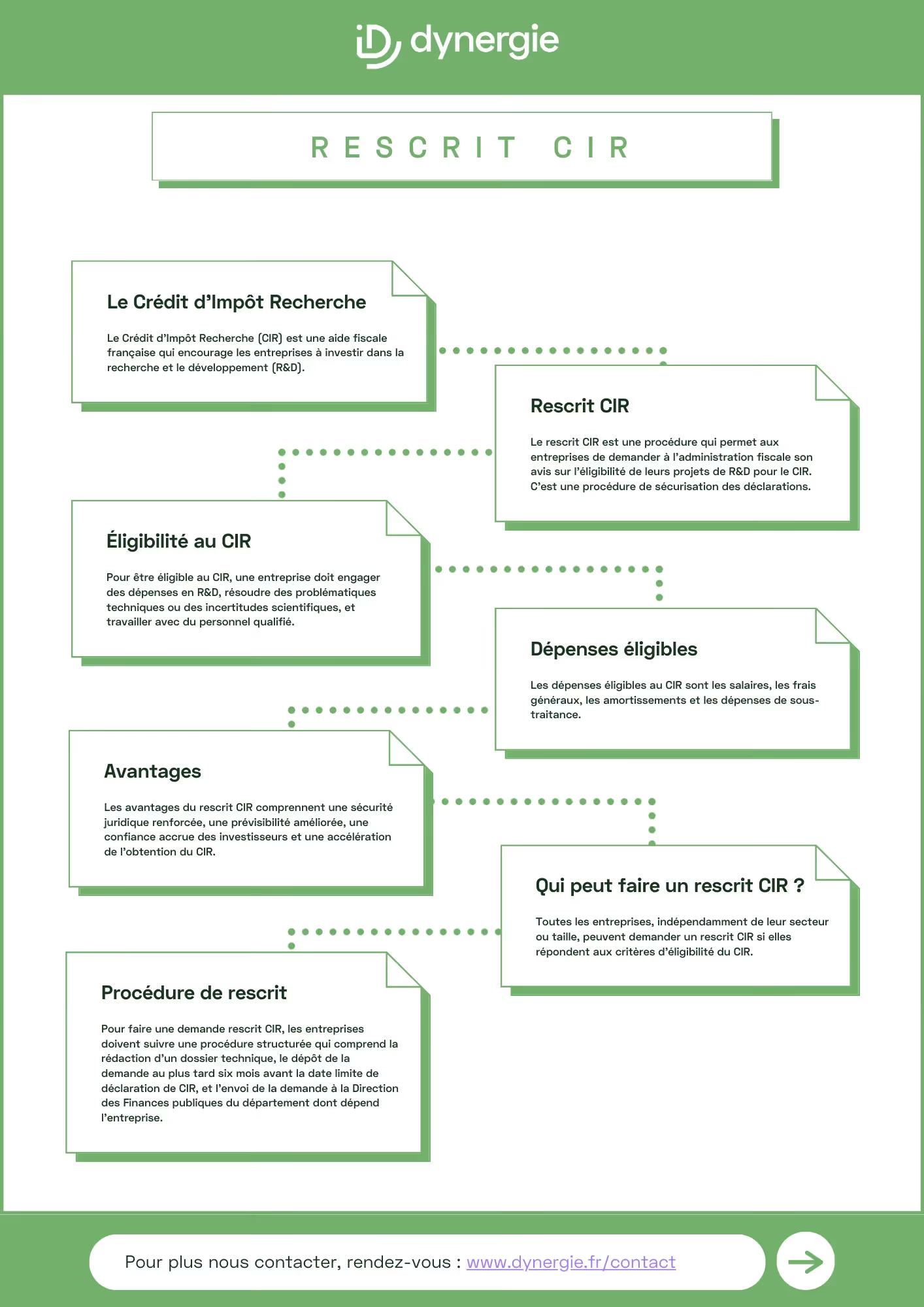

The Research Tax Credit (CIR) is a tax incentive designed to encourage French companies to invest in research and development (R&D). Since its launch in 1983, the CIR has become a pillar of the French economy, benefiting more than 25,000 companies each year.

Given its complexity and the financial stakes involved, the CIR advance ruling procedure was established. It provides companies with legal certainty regarding the eligibility of their R&D projects. This guide explains what an CIR advance ruling is, why it matters, and how companies can use it to optimize and secure their research tax credit.

Definition: What is a CIR tax ruling procedure?

The tax ruling for the Research Tax Credit (CIR) is a procedure that allows a company, for a given tax year, to request the tax authorities’ opinion regarding the eligibility of its research and development (R&D) projects under the CIR.

This is therefore a procedure designed to ensure the security of the declarations.

Through this process, the company receives an official and formal interpretation regarding the application of tax rules specific to its R&D activities.

By obtaining an advance ruling, companies can ensure that their projects meet the eligibility criteria for the CIR. This helps avoid surprises during future tax audits.

However, even if the ruling is favorable, a CIR ruling does not preclude an audit of the accounting information included in the CIR return filed by the company.

How can I qualify for the Research Tax Credit?

To be eligible for the Research Tax Credit (CIR), a company must incur research and development (R&D) expenses. These expenses must meet specific criteria.

Eligible activities must address technical challenges or scientific uncertainties. Current knowledge must not provide an obvious solution to these issues. The work must be innovative and not merely replicate or adapt existing technologies.

To qualify for the CIR, the work must be carried out by qualified personnel. These are often PhDs, engineers, or other professionals with equivalent technical expertise. It should be noted that the CIR can facilitate the hiring of recent PhD graduates.

Eligible expenses may include salaries, overhead costs, depreciation, and subcontracting expenses. Subcontracting must be with approved public or private entities.

What are the benefits of the CIR ruling?

The use of CIR rulings under the Research Tax Credit (CIR) offers several significant benefits for businesses.

First, it provides greater legal certainty. By receiving official confirmation from the tax authorities regarding the eligibility of their R&D projects before reporting their expenses, companies can avoid the risk of a potential tax assessment at a later date.

Second, the advance ruling promotes predictability. It allows companies to plan their R&D investments with a clearer understanding of the financial support they will receive through the CIR. The ruling expands the scope of the CIR (by allowing projects or expenses to be claimed under the CIR that could not have been claimed without prior official approval from the tax authorities); it also enables more effective management of cash flow and project budgets.

Third, a tax ruling can boost investor confidence. Companies that secure their tax position through a tax ruling demonstrate a serious commitment to compliance and sound management. This is an asset when seeking external financing.

Finally, the advance ruling can speed up the process of obtaining the CIR. By clarifying the eligibility of expenses in advance, the tax authority’s review process can be expedited once the return is filed. This allows for faster access to the intended tax benefits.

Which companies are eligible to apply for a CIR ruling?

All businesses, regardless of their type or size, may apply for a CIR ruling if they meet the CIR eligibility criteria.

There are no sector-specific restrictions. Whether the company operates in the technology, pharmaceutical, agricultural, or even creative industries, it is eligible for the CIR ruling.

How do I apply for the CIR through a ruling in France?

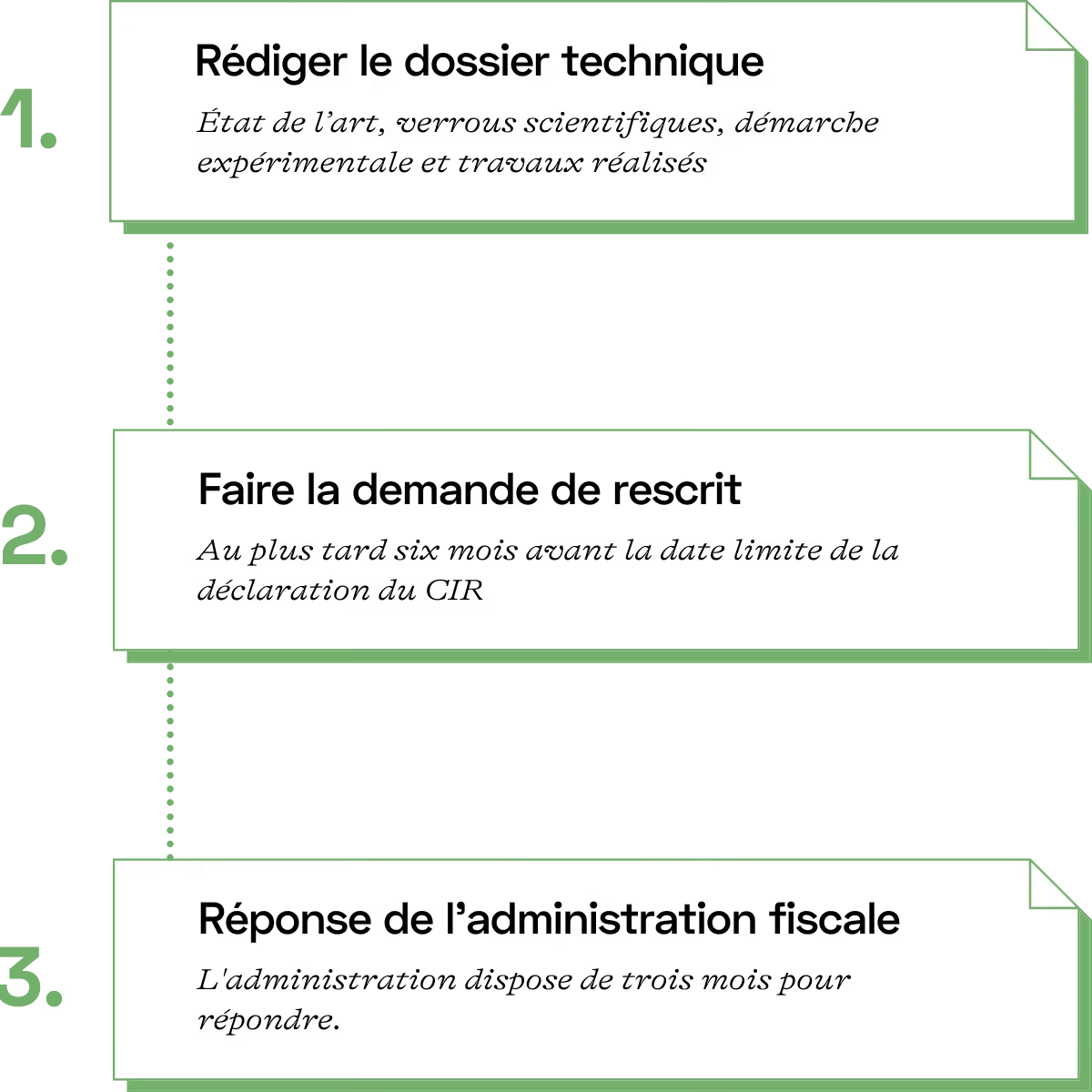

To apply for a Research Tax Credit (CIR) ruling in France, companies must follow a structured procedure that includes several key steps:

File

The content of the CIR ruling varies depending on your request.

To verify your eligibility, you must prepare a technical proposal. This proposal must include a review of the current state of the art, the scientific challenges, the experimental approach, and the work carried out, along with the names of the principal investigators.

The government may request this file up to three years after the CIR filing.

If you are seeking approval for expenses, the ruling must also specify those expenses.

Deadline

The application for a ruling must be filed no later than six months before the filing deadline for the Research Tax Credit (CIR) return for the relevant tax year.

This allows you to obtain a response from the tax authorities before finalizing the return.

Deposit

The application must be submitted to the Departmental Directorate of Public Finance (DGFiP) with jurisdiction over the company.

Companies must ensure that all information provided is accurate and complete. This prevents any delays or the need for clarification that could affect the processing time of the application.

Once the application has been submitted, the government has three months to respond. If it does not respond within that time frame, the decision is deemed to be favorable. This allows the company to proceed with some confidence when claiming its tax credits.

Dynergie, the firm that assists with filing CIR rulings

Dynergie is a certified CIR/CII consulting firm and can assist you in obtaining a tax ruling to ensure the best possible protection for your CIR.

Related articles

Damien Villiers-Moriamé

I assist innovative companies of all sizes in securing public funding (CIR-CII, JEI, bpifrance, CIN, etc.). My technical expertise spans a variety of fields, including IoT, AI, e-learning, embedded systems, and service robotics. My daily work involves supporting entrepreneurs through key and critical stages of their projects (developing a financing plan, creating a business plan, and validating the business model).