2025 Overview of Tax Incentives for Innovation

“How can you reduce the cost of your innovation through tax incentives?” If you’re an innovative company, you’ve surely asked yourself this question before. You’ll find the answer in this article, which provides an overview of the main programs available.

What is a tax incentive for innovation?

In France, tax incentives for innovation projects constitute a specific category of public aid offered by the French government, enabling eligible companies to obtain significant tax relief (tax credits, exemptions, or reductions) and other benefits.

Why is the French government implementing these tax incentives for innovation?

Innovation support programs differ based on the type of assistance they provide, such as: research support, product development support, incentives for collaboration, or commercialization of results.

These programs enable innovative French companies to reduce their project costs, improve their cash flow, and enhance their competitiveness. The government is thus seeking to encourage innovation and research and development (R&D) activities.

What types of innovative companies are eligible for these tax incentives?

Currently, all French companies engaged in innovation or R&D activities are eligible for at least one of the tax incentive programs. However, not every company is necessarily eligible for all of these programs, as they each have distinct eligibility criteria.

What are the main tax incentives for innovation?

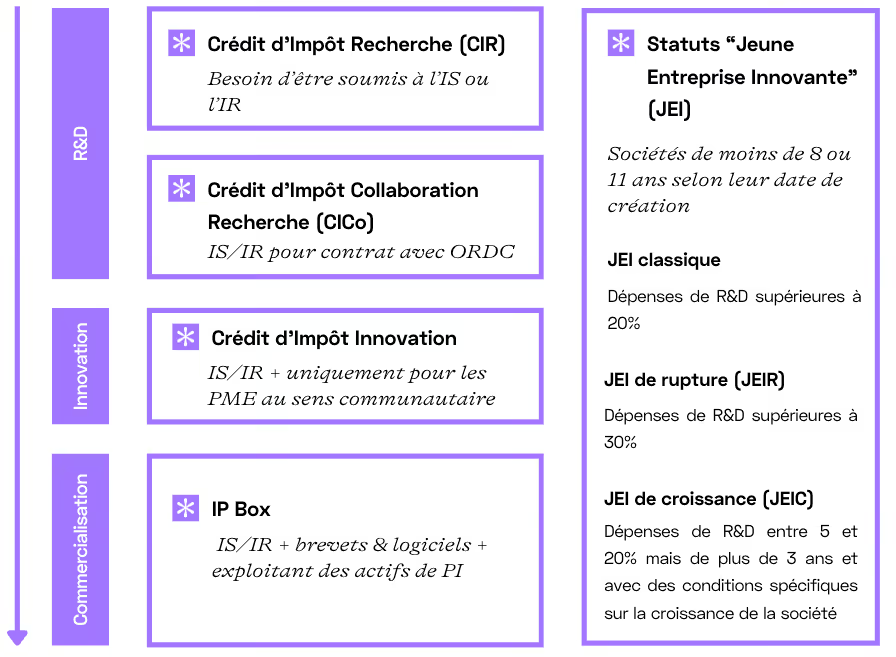

The main tax incentives in France include the Research Tax Credit (CIR), the Innovation Tax Credit (CII), the Research Collaboration Tax Credit (CICo), the Young Innovative Company (JEI, JEIC, JEIR) status, and the IP Box tax regime.

Tax Credits for R&D and Innovation

Research Tax Credit (CIR)

The Research Tax Credit (CIR), the first such program to be established among those presented, is available to all companies subject to taxation in France (corporate income tax or individual income tax).

It allows companies to claim a 30% tax credit (with specific rates in the French overseas departments and Corsica) on their eligible expenses (up to a limit of €100 million; above that amount, the rate is 5%) for basic research, applied research, or experimental development, in accordance with the criteria set forth in the Frascati Manual.

Research Collaboration Tax Credit (CICo)

Introduced in 2022, the CICo offers eligible companies a 40% tax credit (or 50% for SMEs) on R&D expenses incurred under a collaboration agreement with an accredited ORDC (Research and Knowledge Dissemination Organization).

As with the CIR, projects must meet the R&D criteria set forth in the Frascati Manual.

Eligibility is limited to invoices issued at cost by the ORDC, with an annual spending cap of 6 million euros.

Innovation Tax Credit (CII)

The CII, which is exclusively available to SMEs as defined by the European Union, allows companies to recover up to 20% (with specific rates in the French overseas departments and Corsica) of expenses related to bringing new products to market, not just for the company itself.

Projects must involve the creation of new tangible goods that offer a significant improvement in performance in at least one of the following areas— technical performance, eco-design, ergonomics, or functionality —compared to competitors in the market.

"Young Innovative Company" Status

The standard designation: Young Innovative Company (YIC)

The JEI status is intended for SMEs that were established from scratch, are subject to taxation in France, and are less than 8 years old (or less than 11 years old if established before 2023). They must allocate at least 20% of their expenses to R&D activities.

It provides access to exemptions from payroll taxes on R&D salaries, as well as partial exemptions from corporate income tax and certain local taxes, subject to certain conditions. The status can be secured through a tax ruling, similar to the CIR and CII schemes.

The designation for disruptive technology companies: Young Innovative Disruptive Company (JEIR)

The JEIR status is an extension of the JEI status, designed for SMEs—typically deep-tech companies. The company must be eligible for JEI status but must also meet a stricter criterion: at least 50% of its operating expenses must be allocated to R&D activities.

This status entitles investors to an income tax deduction of up to 50% of the amount invested , subject to an annual cap. The JEIR aims to enhance the financial appeal of disruptive companies by facilitating their access to private financing.

The designation for high-growth companies: Young Innovative Growth Company (JEIC)

The JEIC status is aimed at innovative, fast-growing SMEs. To qualify, a company must meet the JEI criteria but, in this case, have R&D expenses accounting for between 5% and 15% of its total expenses and demonstrate a 100% increase in headcount (and an additional 10 FTEs) compared to the fiscal year before last.

This status allows companies to continue enjoying the benefits of the JEI while incurring lower R&D expenses.

The IP Box

The IP Box is a tax regime that allows companies subject to corporate income tax to benefit from a reduced rate of 10% on activities related to the exploitation of certain intellectual property assets (patents, software, trademarks).

This program, which complements the CIR, helps companies commercialize the results of their R&D. Implementing it requires specialized expertise to calculate eligible revenue.

How can you reduce the cost of your innovation through tax incentives?

To make the most of these tax incentives when financing your innovation and R&D projects, it is necessary to follow a specific methodology.

Step 1: Identify the relevant systems and work

Since every business has its own unique characteristics (activities, priorities, constraints, etc.), start by assessing which programs are appropriate for your situation and clearly identify the eligible projects, expenses, or assets.

Step 2: Verify your eligibility

Conduct a thorough review of regulatory criteria: Do your projects meet the tax definition of R&D or innovation? Are your intellectual property assets sufficiently protected for the IP Box? Do your financial and HR metrics qualify you for JEI/JEIC status? etc.

Step 3: Streamline your internal processes

To ensure compliance, implement reliable processes for administrative tracking, cost allocation, technical project traceability, and intellectual property contract management. These elements are critical in the event of a tax audit.

Step 4: Perform the calculations, provide supporting documentation, and file the report

Once you have defined your scope and established your processes, perform an accurate valuation of the amounts involved (calculate tax credits, estimate the IP Box tax base, project JEI/JEIC benefits), compile your technical and financial supporting documentation, and then file your return by the deadline. Note that in some cases, a proactive approach is beneficial for securing the work and expenses through a tax ruling.

We strongly recommend that you engage a financial consulting firm such as Dynergie to handle this work. Since this process is often complex, working with experts provides peace of mind in the event of a tax audit.

Check out our guide to tax incentives for innovation

Excerpt from our comprehensive guide to financing innovative companies: find everything you need to understand and effectively utilize tax incentives for innovation in France, all in one document.

Key concepts to understand when discussing tax incentives for innovation

R&D eligible for the CIR and CICo

The definition of R&D used to determine a company’s eligibility for the Research Tax Credit and the Collaborative Research Tax Credit is based on the criteria set forth in the Frascati Manual (OECD). The manual defines R&D activity as work that meets five conditions: novelty, creativity, uncertainty, systematization, and reproducibility.

The Frascati Manual

An OECD reference document that establishes the methodology for identifying and measuring R&D activities.

The current state of scientific knowledge

A summary of existing knowledge on a given topic, serving as a reference to demonstrate the novelty of an R&D project for the purposes of the Research Tax Credit (CIR).

Innovation eligible for the CII

The Innovation Tax Credit (CII) defines innovation as the creation of a new product that stands out from existing solutions through a significant improvement in performance in one of the following areas: technical performance, eco-design, ergonomics, or functionality.

Market Conditions

For the CII, this analysis identifies existing products and solutions to demonstrate the innovative nature of a new product. It outlines the performance improvements achieved in at least one of the aforementioned areas.

The BOFiP

The Official Bulletin of Public Finance constitutes the official doctrine of the tax administration. It clarifies the interpretation of statutory provisions, particularly with regard to the CIR and the CII.

CIR/CII Tax Credit

Authorization issued by the Ministry of Higher Education and Research for the CIR, or by the Ministry of Industry for the CII, allowing a service provider (public or private) to be authorized to carry out R&D or innovation work eligible for the CIR or the CII.

Tax Ruling on CIR/CII and JEI

An official request submitted to the authorities seeking a written determination regarding a project’s eligibility for the CIR or CII tax credits, or a company’s eligibility for Young Innovative Company (JEI) status.

See our guide to tax incentives for innovation on the next page.

Related articles

Damien Villiers-Moriamé

I assist innovative companies of all sizes in securing public funding (CIR-CII, JEI, bpifrance, CIN, etc.). My technical expertise spans a variety of fields, including IoT, AI, e-learning, embedded systems, and service robotics. My daily work involves supporting entrepreneurs through key and critical stages of their projects (developing a financing plan, creating a business plan, and validating the business model).