Insight: Innovative Young Company (IYC) Status

In this article, we take an in-depth look at what JEI status entails. Whether you’re a startup, an SME, or simply interested in the world of innovation, this guide is for you.

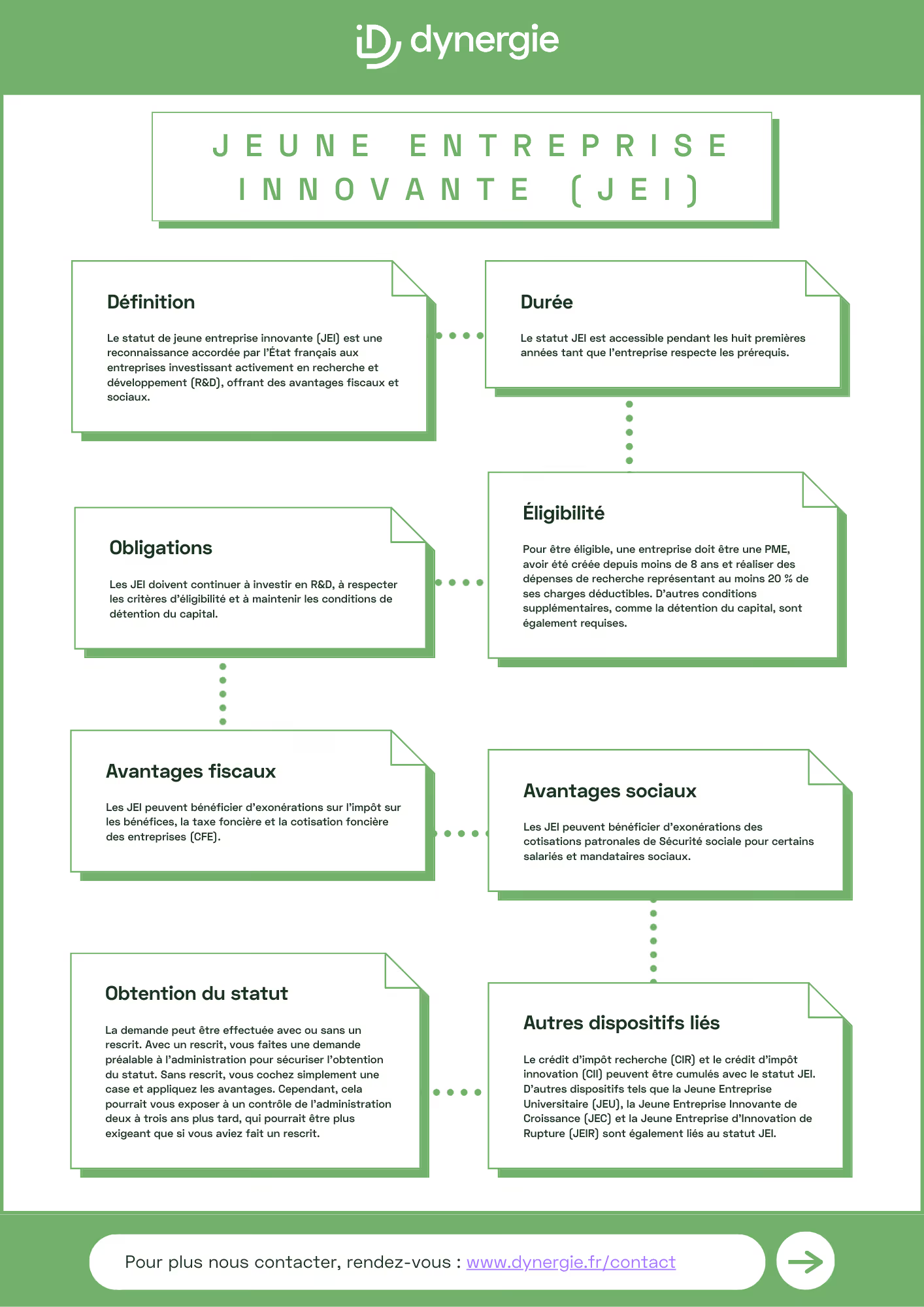

Definition: What is the "young innovative company" status?

The status of Young Innovative Company (YIC) is a designation granted by the French government to companies that actively invest in research and development (R&D). It is designed to support startups and small and medium-sized enterprises (SMEs) by offering them tax and social security benefits.

Duration of Young Innovative Enterprise (YIE) status

The status of a young innovative company (YIC) is available for the first eight years following the company’s incorporation and the start of its first year of operations, provided the company continues to meet the requirements for this status.

It is important to note that this period may vary depending on certain specific criteria; for example, for companies undertaking large-scale research projects or demonstrating strong growth potential.

What benefits is a Young Innovative Company (JEI) entitled to?

Tax Exemptions

Among the tax exemptions available to JEIs are, in particular:

Income Tax Exemption: Businesses are partially or fully exempt from corporate income tax for their first profitable fiscal years. (This exemption will be eliminated for businesses established on or after January 1, 2024.)

Property tax exemption: Young Innovative Enterprises (JEIs) may be eligible for a property tax exemption for a specified period, generally seven years, provided that the local government in question has approved the exemption.

Exemption from the Business Property Tax (CFE): Businesses may also be eligible for a CFE exemption during the same period as the property tax exemption, under the same conditions.

Employee Benefits

In addition to tax exemptions, innovative startups (JEIs) also benefit from social benefits that help support their development and growth:

Exemption from employer Social Security contributions: Employers may be eligible for an exemption from employer Social Security contributions and family allowances for employees assigned to research and development projects. This exemption applies to compensation paid to certain types of employees, such as research engineers, technicians, R&D project managers, etc., provided they devote at least 50% of their working time to these activities.

Exemption for corporate officers: Corporate officers of Young Innovative Companies (JEIs) may also be exempt from employer contributions to Social Security and family allowances if they are primarily involved in the company’s research and development activities.

Eligibility: How do I know if my company qualifies for the JEI?

What are the main criteria?

Here are the main criteria to consider when determining eligibility for JRE status:

1. Company size: The company must be a small or medium-sized enterprise (SME), meaning it must have fewer than 250 employees and generate annual revenue of less than €50 million, with total assets of less than €43 million.

2. Age of the business: The business must have been established less than 8 years prior to the date of its actual incorporation. It must not have resulted from a merger, restructuring, expansion of pre-existing operations, or the takeover of pre-existing operations.

3. Research and development (R&D) expenses: The company must incur research expenses representing at least 20% of its deductible expenses during the fiscal year in which they are incurred. At least 10% of these expenses must be directed or directly controlled by specific individuals, such as students, recent graduates, or individuals engaged in teaching or research activities.

What are the additional requirements?

In addition to the main criteria, there are additional requirements that the company must meet to qualify for Young Innovative Company (YIC) status:

Continuous ownership: At least 50% of the company’s equity must be continuously held by individuals, another company that meets the defined criteria, another JEI, associations or foundations recognized as being of public benefit, venture capital firms, investment funds, or other specific entities.

Engaging in a new business activity: The company must be a newly established business, not resulting from a merger, restructuring, expansion, or takeover.

These additional criteria, combined with the main criteria, help determine whether a company is eligible for the status of a young innovative company (YIC) and can benefit from the associated advantages.

What are the obligations associated with JEI status?

By qualifying as a Young Innovative Company (YIC), the company agrees to comply with certain requirements:

Continuation of R&D Activities: The company must continue to invest in research and development (R&D) activities in order to maintain its status as a Young Innovative Company (YIC). This often requires dedicating a significant portion of its resources to these activities, in accordance with the criteria established for obtaining this status.

Compliance with eligibility criteria: The company must continue to meet the eligibility criteria established for JEI status. This includes maintaining its status as a small or medium-sized enterprise (SME), complying with revenue and balance sheet limits, and maintaining the required percentage of R&D expenses relative to deductible expenses.

Maintenance of capital ownership requirements: The company must also ensure that the capital ownership requirements, as defined for obtaining JEI status, are maintained. This means that at least 50% of the capital must continue to be held on a continuous basis by the shareholders specified by law.

Connection to other systems

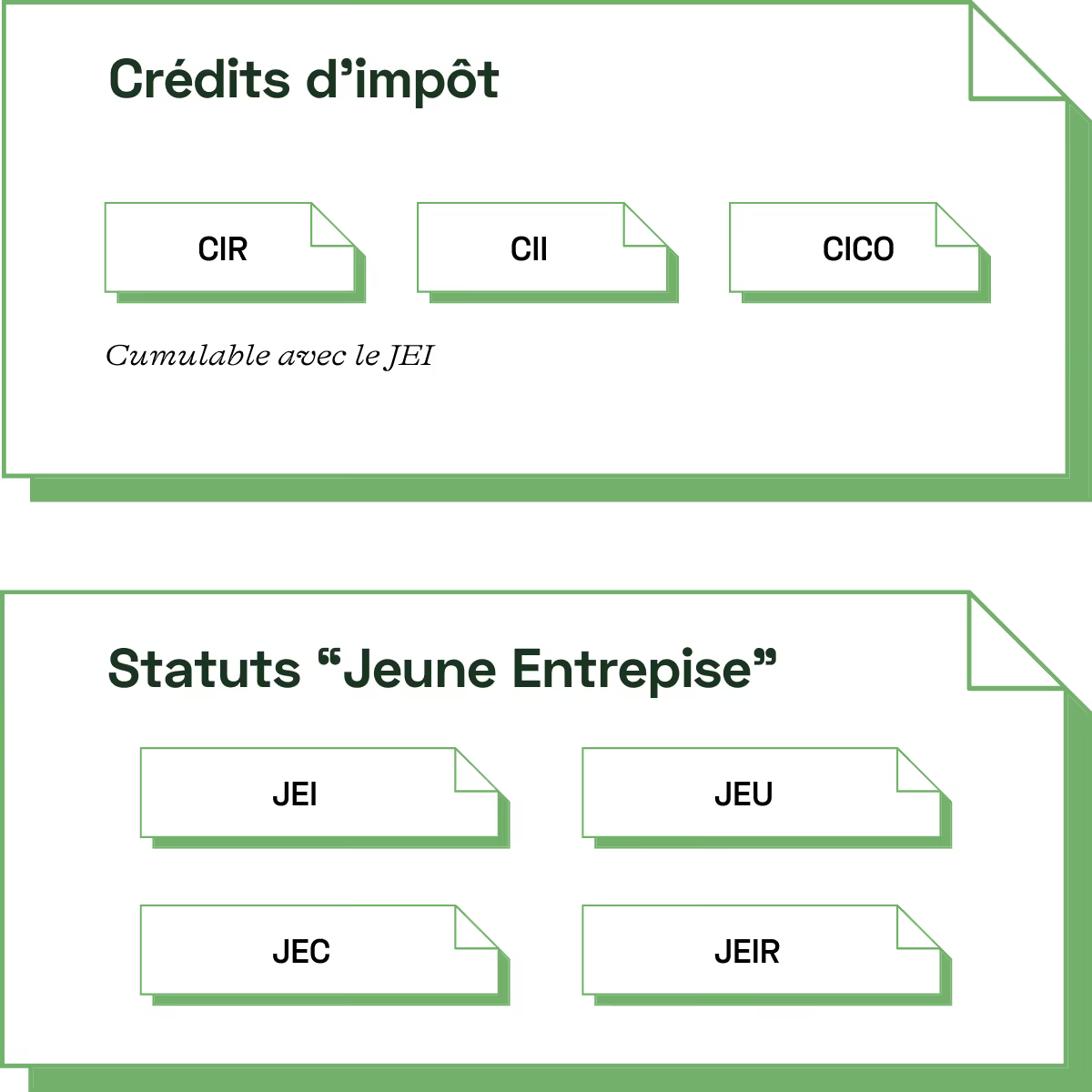

Research Tax Credit (CIR) & Innovation Tax Credit (CII)

The Research Tax Credit (CIR) and the Innovation Tax Credit (CII) are two key tax incentives that can be combined with the status of a young innovative company (JEI).

The Research Tax Credit (CIR): The JEI status offers tax and social security benefits to companies engaged in research and development (R&D). The CIR, meanwhile, allows companies to recover a portion of their R&D-related expenses in the form of a tax credit. Thus, a company with JEI status can take advantage of both the JEI and CIR benefits to support its R&D activities.

Innovation Tax Credit (CII): The CII is designed to encourage innovation activities that take place prior to the commercialization of a new product. This program can be combined with other tax incentives, such as the JEI status and the CIR. However, it should be noted that the eligible activities are fundamentally different from those eligible for the CIR.

University-Based Startup (UBS)

The University-Based Start-up (JEU) is a specific program designed to support companies created as a result of research conducted at higher education institutions or public research laboratories. Unlike the JEI status, which is intended for all innovative start-ups, the JEU specifically targets companies originating from the academic sector.

To qualify for JEU status, the company must meet the following criteria:

- Recognize research work in which executives or partners have participated at a higher education institution authorized to award a degree conferring at least a master’s degree.

- Have close ties to a university or a public research laboratory.

- A young company, often newly established, generally less than 8 years old.

- Allocate a significant portion of its budget to research and development.

The benefits available to companies with JEU status are similar to those of JEI status, including tax exemptions, financial assistance, and simplified access to certain innovation support programs.

Young Growth Innovation Company (JEIC) & Young Disruptive Innovation Company (JEIR)

The new JEIC and JEIR tax statuses, mentioned in the Midy report, represent a significant development in the landscape of tax incentives for innovative companies:

Young Innovative Growth Company (JEIC) : This status applies to growing companies that spend between 5% and 20% of their revenue on R&D. It aims to support SMEs that demonstrate strong potential for growth and innovation but do not fully meet the strict criteria for JEI status. In return, they must demonstrate strong growth potential, with specific indicators to be defined by decree.

Young Innovative Disruptive Company (JEIR) : JEIRs are recently established companies (less than 12 years old) that devote more than 30% of their expenses to R&D. This status is designed to help companies conduct more ambitious research and invest more in disruptive innovation by providing them with the means to finance their activities, which are more costly. To this end, JEIRs benefit from enhanced tax incentives to stimulate private investment in their favor.

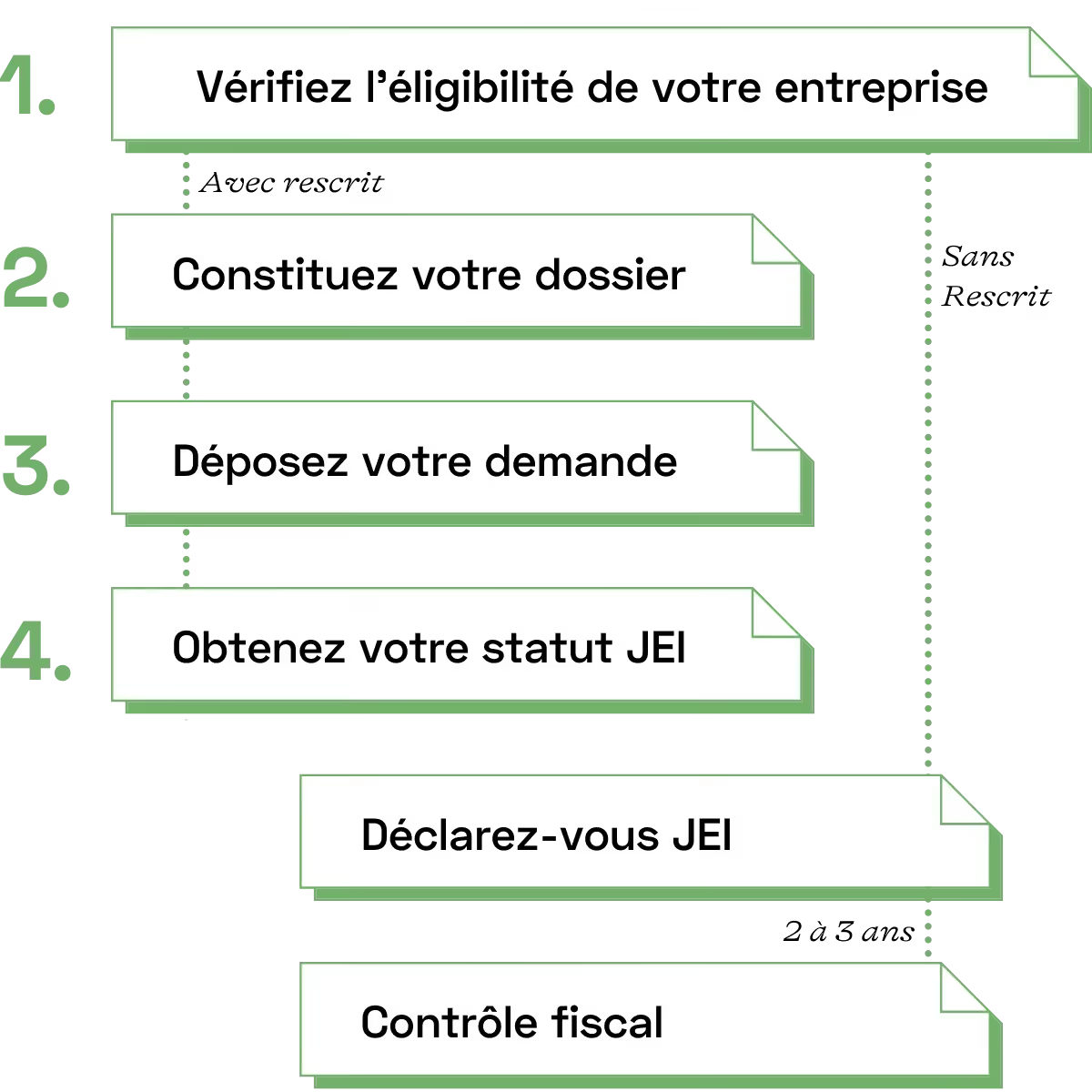

How do I apply for and obtain JEI status?

Application Process for Young Innovative Enterprise (YIE) Status

The application can be submitted with or without a ruling. With a ruling, you submit a request to the tax authorities in advance to ensure you qualify for the status. Without a ruling, you simply check a box and claim the benefits. However, this could expose you to a tax audit two to three years later, which might be more rigorous than if you had obtained a ruling.

Here are the steps to follow, as outlined in the ruling:

1. Check your company’s eligibility: Before applying, make sure your company meets the criteria required to obtain JEI status. These criteria include being an SME, having been in operation for less than 8 years, and allocating at least 20% of its expenses to research and development (R&D).

2. Prepare your application: Gather all the necessary documents to support your application, such as proof of your revenue, R&D expenses, and the date your business was established.

3. Submit your application: Once your application is complete, you can submit it to the appropriate tax authority. Be sure to follow the instructions provided by the authority and include all required information.

4. Obtain your JEI status: If your application is approved, you will receive an official notification granting you Young Innovative Company (JEI) status. You will then be eligible for the tax and social security benefits associated with this status for a limited period.

If you decide to take the risk of a tax audit 2 to 3 years down the line and therefore file your return without a tax ruling, as mentioned earlier, you simply need to register as a JEI with the tax authorities and apply the tax and social security benefits.

The JEI ruling

The JEI ruling is an administrative procedure that allows companies to request confirmation from the tax authorities that they are eligible for Young Innovative Company (JEI) status. In other words, it is an official request submitted to the tax authorities to obtain a formal determination that the company meets the criteria required to qualify for the tax and social security benefits associated with JEI status.

This approach is of great importance to businesses, as it offers several advantages:

1. Legal certainty: By obtaining an official response from the tax authorities, the company receives formal confirmation of its eligibility for JEI status. This provides significant legal certainty, as the company can rely on this decision in the event of a future tax audit.

2. Tax Optimization: The JEI status offers significant tax benefits, such as tax exemptions on profits and payroll taxes. By obtaining confirmation of its eligibility through a tax ruling, the company can plan its operations and investments with full knowledge of the facts, thereby maximizing the tax benefits it is entitled to.

3. Time savings: The advance ruling provides a clear and prompt response from the tax authorities regarding the company’s eligibility for JEI status. This avoids the uncertainty and delays associated with other methods of verifying eligibility, allowing the company to focus on its core business activities.

Practical tips for maximizing the benefits of JEI status

To maximize the benefits of JEI status, here are some practical tips:

1. Plan your R&D expenditures: Since JEI status requires your company to allocate at least 20% of its expenditures to research and development (R&D), it is essential to plan these investments strategically. Identify the priority R&D projects that will contribute most to your company’s innovation and growth.

2. Keep accurate records: To fully benefit from the tax advantages of JEI status, you must keep accurate records of all your R&D expenses. This includes salaries for employees working on R&D projects, subcontracting costs, expenses related to equipment and materials, as well as other costs associated with research and development.

3. Be proactive with your administrative procedures: To avoid any delays in obtaining JEI status, be sure to submit your application as soon as your company meets the eligibility criteria. Be prepared to provide all the necessary documents and information to support your application.

4. Consult with experts: If you have questions or concerns about your eligibility for JEI status or how to maximize its benefits, don’t hesitate to consult with tax experts or consultants who specialize in this area. Their expertise can help you make informed decisions and optimize your tax strategy.

5. Stay informed about legislative changes: Tax regulations and the eligibility requirements for JEI status may change over time. It is therefore essential to stay informed about the latest legislative updates and adapt accordingly to continue fully benefiting from the advantages of JEI status.

Dynergie, a firm that helps you obtain and maintain JEI status

Dynergie can assist you in obtaining and maintaining your JEI status. If you would like to take advantage of our expertise, you can view our services here.

Useful links:

Related articles

Damien Villiers-Moriamé

I assist innovative companies of all sizes in securing public funding (CIR-CII, JEI, bpifrance, CIN, etc.). My technical expertise spans a variety of fields, including IoT, AI, e-learning, embedded systems, and service robotics. My daily work involves supporting entrepreneurs through key and critical stages of their projects (developing a financing plan, creating a business plan, and validating the business model).