A Guide to Tax Credits for Innovative Businesses in 2025

In the world of tax incentives for innovation, the category of “Tax Credits” can be complex. This article will provide you with all the information you need to better understand the various programs, their eligibility requirements, as well as the rates and recoverable amounts.

What is a tax credit for innovative companies? - Definition

A tax credit for innovative companies is a tax incentive established by the French government that provides a tax reduction for innovation and research and development (R&D) activities.

Programs of this kind cover a wide range of activities: basic research, prototyping and design of innovative products and services, production, and so on.

Through these "tax credits," the government aims to reduce the tax burden on companies in order to encourage them to invest more in their innovation activities.

What tax credits are available for innovative companies?

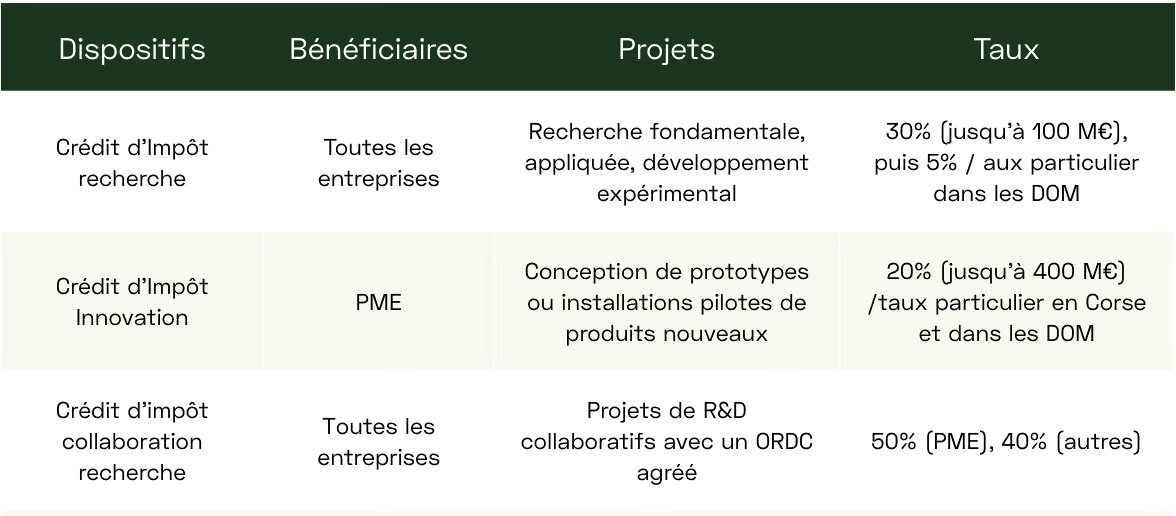

The main tax credit programs available to innovative companies are:

- The Research Tax Credit (CIR)

- The Innovation Tax Credit (CII)

- The Research Collaboration Tax Credit (CICo)

There are other tax credits available to businesses, such as the Collection Tax Credit (CIC). However, these programs will not be discussed in this article, as they are too far removed from the fields oftechnological/scientific innovation and research.

Research Tax Credit (CIR)

Created in 1983, the Research Tax Credit is designed to encourage companies to invest specifically in research and development (R&D) by allowing them to recover a portion of their expenses.

All businesses are eligible if they are subject to the actual tax regime (standard or simplified) forcorporate income tax (CIT) orindividual income tax (IIT), regardless of their size or industry.

Generally speaking, it is possible to recover a portion of eligible expenses (such as personnel costs, depreciation of equipment, and approved subcontracting) related to basic research, applied research, or experimental development, in accordance with the definition in the Frascati Manual.

The CIR rate may vary depending on the type of business and geographic region, as well as the amount of research spending. In mainland France, it is currently 30% for spending up to €100 million. Above that amount, the rate drops to 5%. In the overseas departments, the initial rate is 50%.

For more information, visit this page on the Service-Public Entreprendre website.

Innovation Tax Credit (CII)

Created in 2013, the Innovation Tax Credit (CII) is designed to encourage companies to continue investing after the research phase, serving as an extension of the CIR. The two programs can therefore be combined.

Only small and medium-sized enterprises (SMEs) as defined by the European Union are eligible if they are subject to corporate income tax or income tax (even if they do not pay any).

SMEs, as defined by the European Union, are companies with fewer than 250 employees as of the balance sheet date, with annual revenue not exceeding €50 million or total assets not exceeding €43 million.

The CII allows eligible companies to receive a tax benefit on expenses related to personnel, depreciation, approved subcontracting, or intellectual property associated with prototype projects or the development of pilot facilities for new products or services.

These projects must not yet be available on the market and must stand out from existing products through superior performance in terms of technical specifications, eco-design, ergonomics, or functionality.

The CII rate varies depending on the region or the size of the company:

- 20% in mainland France

- 60% in the overseas departments

- 40% for small businesses in Corsica

- 35% for medium-sized companies in Corsica

Please note that in all cases, the total eligible expenses may not exceed €400,000.

For more information, visit this page on the Service-Public Entreprendre website.

Research Collaboration Tax Credit - CICo

Created in 2022 by the Finance Act, the Research Collaboration Tax Credit (CICo) is designed to encourage companies to engage in R&D activities in partnership with research and knowledge dissemination organizations (ORDCs).

An ORDC is an independent entity that conducts basic, industrial, or experimental research and disseminates its findings through teaching or publications, according to the European Commission’s State Aid Guidelines (university, research institute, or technology transfer agency). Note that the ORDC research partner must be accredited in order to include its expenses in the CICo base.

Eligible beneficiaries of this program are all businesses subject to a full taxation regime (corporate income tax or individual income tax) that have entered into a collaboration agreement with an ORDC. However, they must not be in financial difficulty.

Eligible expenses (equipment, personnel, and operating costs) taken into account are those billed by the ORDC for basic or applied research activities, or for prototype development or pilot plant operations.

The CICo rate is 50% for SMEs and 40% for other entities, up to a limit of €6 million per year.

For more information, visit this page on the Service-Public Entreprendre website.

Key Procedures for Tax Credits for Innovative Companies

Certifications

Under the CIR, CII, and CICo programs, tax approval is an official authorization issued by the government to a business or organization, allowing it to pass on the tax credit to its clients for the work it performs for them.

Rulings

The advance ruling allows companies to verify with the tax authorities whether their projects are eligible for the Research Tax Credit (CIR), the Innovation Tax Credit (CII), and the Research Collaboration Tax Credit (CICo).

This provides legal certainty: if the government approves the request, it cannot reverse its decision during an audit, as long as the described situation remains unchanged.

Tax Credit for Innovative Companies: How to Qualify?

To qualify for these tax credits, you must meet the eligibility requirements and file a claim with the tax authorities. Since the procedures vary depending on the specific program, we recommend consulting an innovation financing advisory firm such as Dynergie.

This will allow you to focus on your innovation projects while benefiting fromexpert guidance to maximize recoverable funds and avoid challenges to your claims.

Related articles

Damien Villiers-Moriamé

I assist innovative companies of all sizes in securing public funding (CIR-CII, JEI, bpifrance, CIN, etc.). My technical expertise spans a variety of fields, including IoT, AI, e-learning, embedded systems, and service robotics. My daily work involves supporting entrepreneurs through key and critical stages of their projects (developing a financing plan, creating a business plan, and validating the business model).