Reforms to the JEI status in the 2024 Budget Act: What remains of the Midy report?

As part of the 2024 Finance Act enacted on December 30, 2023, and following the Midy Report (named after the representative from Paris-Saclay who submitted a report on public investment in innovative SMEs), a reform of the status of young innovative companies has been in effect since January 1, 2024. An in-depth look.

Table of Contents

I. What is the Midy Report?

- A report to counter the slowdown in investment in innovative companies

- Support for innovative SMEs and startups to help them achieve their goals

II. What are the latest developments regarding the JEI status?

- The JEI status: Who is it for?

- What does the reform of the JEI status entail?

- What are these growth potential criteria?

III. Dynergie’s Strategy Regarding Young Innovative Enterprise (JEI) Status

I. What is the Midy Report?

A report to counter the slowdown in investment in innovative companies

The Midy Report, presented to the President of the Republic by Representative Paul Midy at the Vivatech trade show on June 16, 2023, aimed to better understand the slowdown in growth among innovative SMEs and startups and to identify potential areas for improvement.

In fact, the ecosystem of innovative companies in France has seen spectacular growth since 2017:

- The number of unicorns has increased tenfold in five years;

- The number of new businesses has surged by 26% over the past six years;

- the number of jobs created has increased fivefold over the past five years;

- The number of fundraising campaigns has increased more than fivefold over the past five years.

However, the end of 2022 and the beginning of 2023 showed signs of aserious slowdown.¹ The warning signs that began to emerge at the end of last year have recently been confirmed: in 2023, European startups raised €45 billion, compared to €82 billion in 2022—a staggering drop of more than45%2. The trend is the same at the national level: fundraising byFrench startups is down 38% compared to 20223.

And even though the end of the post-COVID “magic money” era pointed to a significant decline (-18% between 2021 and 2022), and while it is important to put the irrational interlude of the post-COVID era into perspective, support for innovative companies remains essential to ensure they can grow as effectively as possible.

Support for innovative SMEs and startups to help them achieve their goals

This focus on SMEs and startups is not insignificant. According to figures from the Midy report and the evaluation of the program conducted by INSEE in2021, they hire more people, create more indirect jobs, and, most importantly, these positions cover the full range of needs in the labor market (unskilled, low-skilled, and skilled jobs) while offering above-average wages.

Preserving, strengthening, and fostering the growth of these innovative companies is therefore essential not only to achieving the goals of full employment and ecological transition today, but also to positioning France as a European leader in the challenges of tomorrow.

This is the spirit in which the Midy Report was presented: support for the growth of all companies capable of innovation and expansion, and strong support for companies driving disruptive innovation—those capable of radically transforming our lifestyles.

II) What are the latest developments regarding the JEI status?

The JEI status: Who is it for?

The status of young innovative company (JEI) is defined inArticle 44 sexies 0-A of the General Tax Code.

According to him, a JEI is therefore:

- An SME with fewer than 250 employees and annual revenue of less than €50 million or total assets of less than €43 million;

- Less than 8 years for companies established after January 1, 2023, and 11 years for companies established before January 1, 2023;

- Independent;

- Truly new (i.e., not resulting from a restructuring, merger, expansion, or takeover);

- A company that spends at least 15% of its total expenses on research OR is managed or at least 10% owned by students or individuals who have held a master’s or doctoral degree for less than five years OR spends between 5% and 15% of its total expenses on research and meets certain economic performance criteria.

The JEI program allows a company to benefit, through the end of its seventh fiscal year, from exemptions from property taxes and levies, but also—and most importantly—from exemptions from employer contributions on compensation paid to employees and corporate officers.

What does the reform of the JEI status entail?

A consultation process lasting more than six months and involving 400 participants yielded numerous recommendations, some of which were incorporated into the 2024 Finance Act. Among those adopted is the expansion of the JEI program to include a greater number of growth-oriented companies so that they may benefit from the exemption from social security contributions. The stated goal of this expansion is to double the number of companies benefiting from the advantages of JEI status.

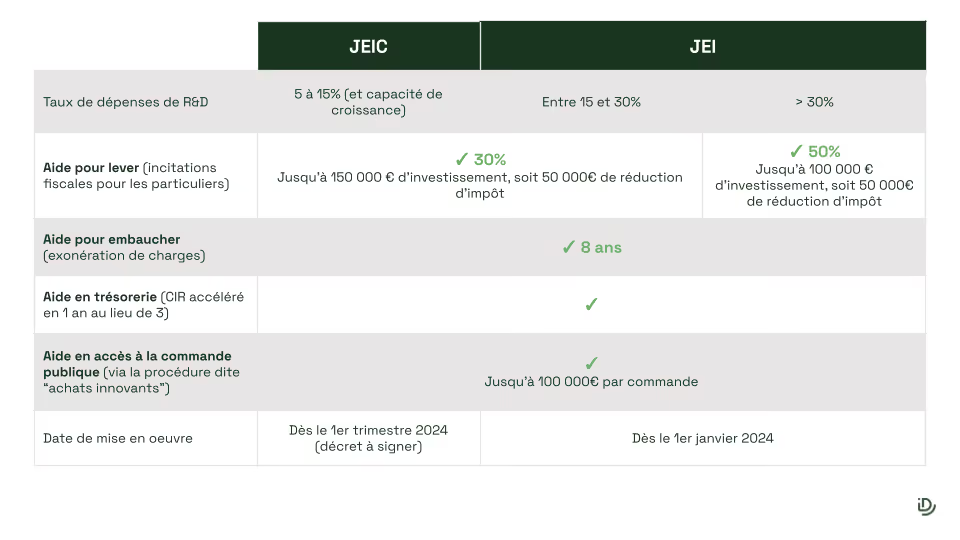

This reform thus opens the program to young innovation and growth companies (JEICs) that incur R&D expenses representing between 5% and 15% of their total expenses and demonstrate strong growth potential (see table below).

⚠️ The 2024 Budget Bill, however, proposes to eliminate the corporate income tax exemption for new Young Innovative Companies (JEIs) established on or after January 1, 2024, even though the program was originally set to remain in effect until 2026, on the grounds that this benefit is no longer relevant.

In addition to this measure, the 2024 Finance Act includes other changes recommended by the report, which focuses on four areas of support and incentives for innovative SMEs and startups:

- Hiring Assistance: Expansion of the Program to Make More Businesses Eligible for Social Security Contribution Exemptions

- Fundraising assistance: tax incentives for individuals investing in JEIs. A 30% tax credit for investments in JEIs/JEICs, and a 50% tax credit for JEIs that allocate more than 30% of their expenses to research

- Cash flow assistance: eligibility for the accelerated CIR (allows you to receive the CIR in 1 year instead of 3)

- Support for accessing public procurement: eligibility for a simplified procedure allowing public buyers (the federal government, local governments, hospitals, etc.) to place orders of up to €100,000 with a Young Innovative Company (JEI) without a competitive bidding process and using a simplified procedure.

“We must continue to ensure that many more startups are created—and funded—each year. That is why we will be working on two fronts. First, we will encourage the financing of innovative companies in their early stages by making our tax system more attractive, drawing inspiration from proven schemes in neighboring countries such as the UK’s EIS/SEIS.” Emmanuel Macron, April 21, 2022

What are these growth potential criteria?

Previously reserved for companies with R&D expenses amounting to at least 15% of their total expenses, the program has been expanded to support more companies and stimulate their growth in the early stages of their development.

The law stipulates that the expansion of the JEI program to include high-growth startups (JEC, or JEIC, depending on the terminology used) is contingent“on economic performance indicators defined in accordance with procedures specified by decree.” According to Representative Paul Midy, this decree is expected to be issued during the first quarter of 2024 to clarify the selected indicators.

Nevertheless, the report produced by the latter provides insight into the content of these indicators. Based on the definitions of startups and innovative SMEs used by INSEE, Bpifrance, and the OECD, two criteria appear to be common:

- Hypergrowth;

- The increase in staff numbers.

While every organization has its own definition of a startup and an innovative SME, these two criteria are common to all definitions. Regarding the capacity for hypergrowth, INSEE defines a threshold of 20% annual revenue growth over three years. As for the capacity to grow its workforce, the OECD considers an SME to be “growth-oriented” if it experiences a 20% increase in its workforce annually over three consecutive years.

These two criteria are therefore the most likely to be included in the decree that will establish the growth indicators for JEC status.

❇️ These measures are expected to generate more than 600 million euros in funding starting in 2024 and create 30,000 to 50,000 jobs over the next five years.

Dynergie's Strategy Regarding JEI Status

The status of innovative start-up is a self-declared status, meaning that companies do not need to provide ex ante proof of compliance with the program’s criteria to qualify. However, the tax authorities conduct thorough audits of companies that self-declare as innovative start-ups.

Dynergie therefore recommends confirming your eligibility for JEI status with the tax authorities through an advance ruling, which allows you to receive the authorities’ opinion on whether you meet the program’s criteria before filing your tax return. Our experts are here to assist you in securing these tax benefits and thereby boosting your company’s growth!

Sources:

1 Paul Midy, Supporting Investment in Startups, Innovative SMEs, and Growth SMEs, Government Task Force, June 2023.

2 Charlie Perreau, Start-ups: Record Drop in Funding Raised in Europe in 2023, Les Échos, published on November 28, 2023. https://www.lesechos.fr/start-up/ecosysteme/start-up-baisse-record-des-montants-leves-en-europe-en-2023-2037528

3 Charlie Perreau, Fundraising in French Tech: After Two Years of Euphoria, the Correction of 2023, Les Échos, published on January 11, 2024. https://www.lesechos.fr/start-up/ecosysteme/levees-de-fonds-dans-la-french-tech-apres-deux-annees-deuphorie-la-correction-de-2023-2045573

4 Simon BUNEL, Clémence LENOIR, and Simon QUANTIN, Evaluation of the Young Innovative Company (JEI) Program: An Example of the Application of the Rosenbaum Sensitivity Analysis Model, Working Papers No. 2021-001 – October 2021, INSEE https://www.bnsp.insee.fr/ark:/12148/bc6p076xd6m/f1.pdf

Related articles

Romain Escriva

Forecasting and Business Intelligence Analyst at Dynergie