Insight: Young University Enterprise (JEU) Status

The Young University Enterprise (JEU) status represents a valuable opportunity for creative and ambitious individuals, whether they are students, recent graduates, or academic staff. This status, which is closely linked to the Young Innovative Enterprise (JEI), offers a fast track for those who wish to launch their own business while enjoying significant benefits. Eligibility requirements, tax and social benefits, application process—discover how the JEU can serve as a springboard for your innovation and entrepreneurship projects.

Definition: University-Based Start-up (JEU)

The University Start-up (JEU) is a legal status reserved for companies founded by students, recent graduates, or academic staff involved in research at institutions of higher education. These companies benefit from specific conditions as well as social and tax advantages, with the aim of encouragingentrepreneurship within the academic community.

What are the requirements to become a JEU?

To be recognized as a Young University Enterprise (JEU), several criteria must be met:

1. Academic involvement: At least 10% of the company’s equity must be owned by stakeholders from the academic community, such as students, recent graduates, or academic staff.

2. Corporate independence: A majority stake ( 50% or more) in the company’s equity capital must not be held by other companies.

3. Company size: The company must have fewer than 250 employees and annual revenue of less than 50 million euros, qualifying it as a small or medium-sized enterprise (SME).

4. Duration: JEU status may only be granted during the first 8 years following the company’s establishment.

5. Link to higher education: The JEU must establish a partnership with a French higher education institution, formalized through an agreement that specifies the nature of the collaboration and the dissemination of research findings.

What are the benefits?

The benefits of the JEU (Young University Enterprise) are numerous and can greatly support the growth of a young university enterprise.

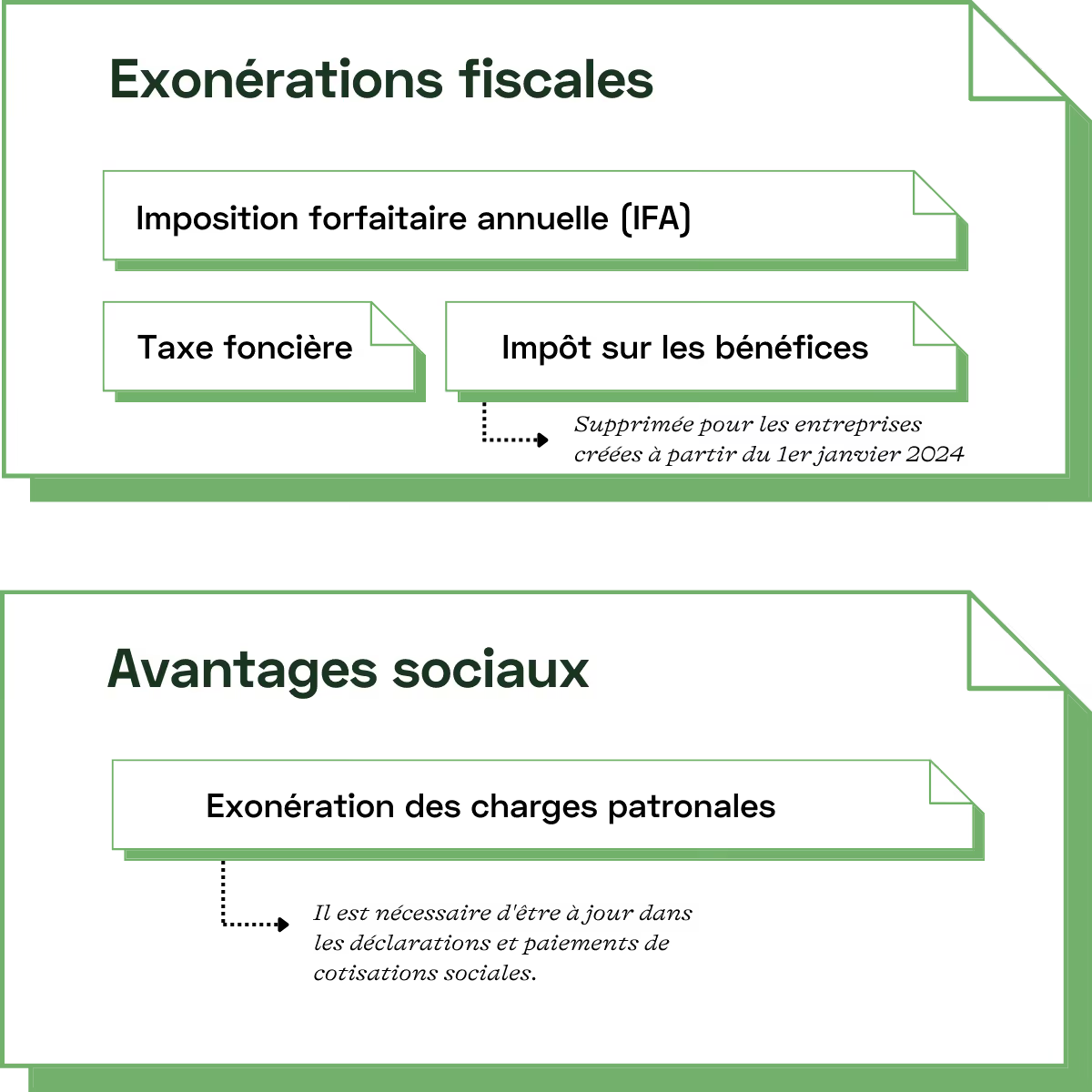

Tax breaks

The tax breaks provided under the Young University Enterprise (JEU) status offer significant benefits to eligible companies. First, these companies are eligible for a full exemption from income tax for their first fiscal year, followed by a 50% reduction for the following fiscal year.

Businesses established after January 1, 2024, will not be eligible for the income tax exemption.

In addition, they may be eligible for a property tax exemption for up to seven years, subject to approval by local authorities. This exemption also applies to the business property tax (CFE).

Finally, the beneficiary company is exempt fromthe annual flat-rate tax (IFA) for as long as it retains its JEU status.

Exemption from employer contributions

The exemption from employer contributions is a significant benefit for companies with Young University Enterprise (JEU) status. This exemption covers several types of social security contributions, including those related to maternity, disability, and death insurance, as well as family allowances and retirement benefits.

It should be noted that this exemption does not cover all social security contributions. It does not include contributions for supplemental pension plans, additional employer contributions, or contributions related to occupational diseases and workplace accidents.

Eligible companies may take advantage of this exemption for a limited period, which may not exceed a maximum of 8 years. In addition, limits have been set for this exemption, particularly regarding the amount of gross wages. Specifically, this exemption is capped at a portion of gross wages less than 4.5 times the minimum wage, and at an annual ceiling based on the social security ceiling.

It is important to note that, to be eligible for this exemption, companies must be up to date with their social security reporting and payments. However, arrangements may be made for companies that have established a plan to settle their social security contributions.

Connection to the JEI (Young Innovative Company) status

The JEU is a variant of the JEI, with each having specific requirements. The JEI is open to any innovative company that meets certain criteria, while the JEU must be at least 10% owned by academic entities.

Each legal status has its own criteria and requirements, which companies must meet in order to qualify for the corresponding benefits. Thus, although the JEU and the JEI share some similarities, they are two distinct legal statuses with their own eligibility requirements.

What is the application process for the JEU?

Steps to follow to obtain status

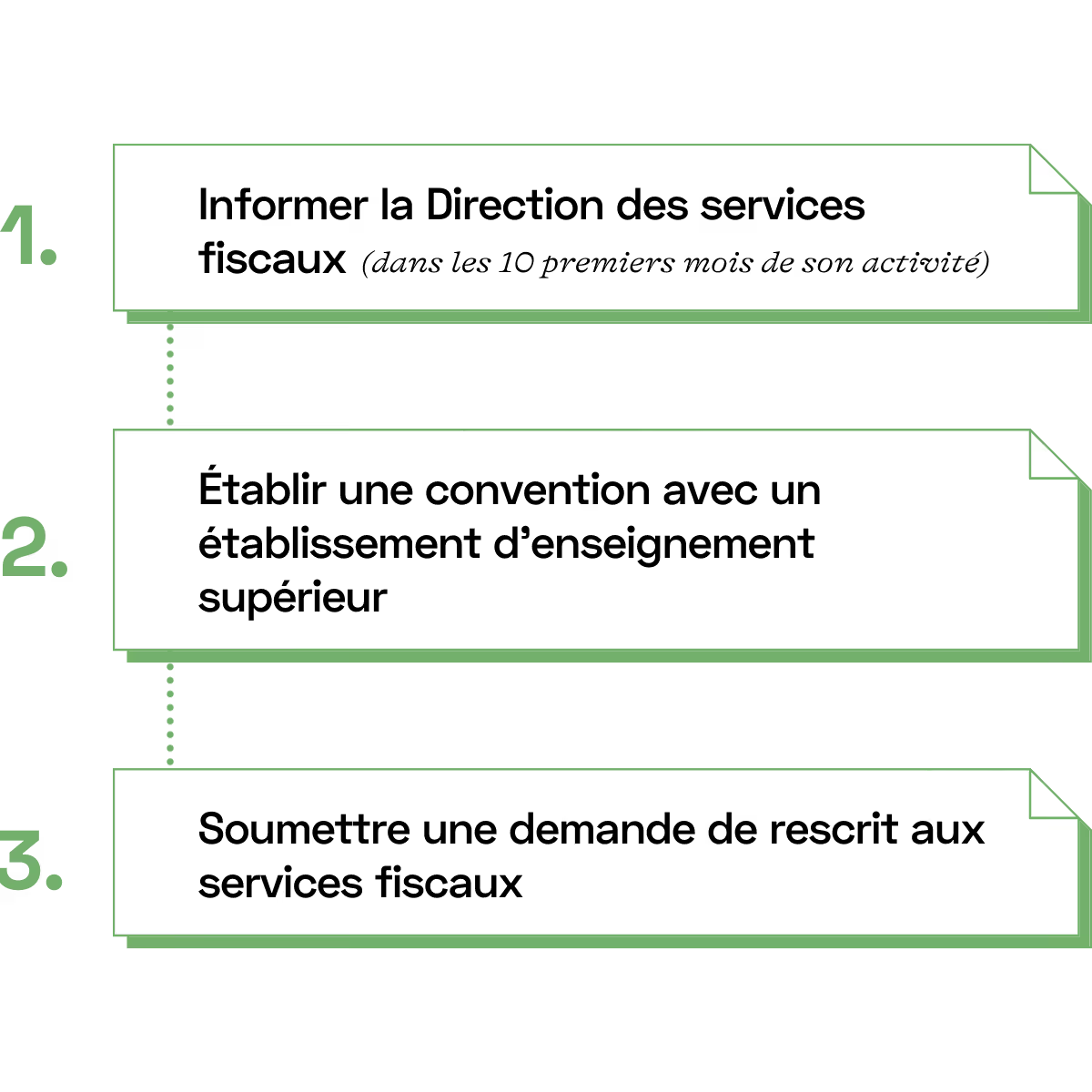

To obtain Young University Enterprise (JEU) status, you must follow these steps:

1. Early notification: You must notify the Tax Services Directorate of your intention to obtain JEU status within the first 10 months of the company’s operations.

2. Agreement with a higher education institution: You must also enter into an agreement with a French higher education institution that outlines the partnership and the dissemination of your research findings.

3. Request for a ruling: You may submit a request for a ruling to the tax authorities to confirm that you meet the required criteria.

The application process can be completed with or without a ruling. A ruling involves submitting a request to the tax authorities in advance to ensure that you qualify for the status. Without a ruling, you simply select an option and enjoy the benefits. However, this approach could leave you vulnerable to a tax audit later on, which might be more rigorous than if you had obtained a ruling.

Contents of the agreement with a higher education institution

The agreement between the company and the institution of higher education must include the following:

- The distribution of ownership of the company among academic stakeholders, with a minimum 10% stake held by members of the academic community.

- A description of the research projects supported by the company.

- Intellectual property associated with research work.

- The services provided by the institution of higher education, such as financial or logistical support.

Renewal and Loss of Status

- Renewal of the agreement: The initial agreement is valid for 3 years and may be renewed for up to a total of 8 years from the date the company was established.

- Loss of status: The company loses its JEU status if it no longer meets the required criteria, particularly if it has been in existence for more than eight years.

JEU Ruling

The JEU ruling gives you the opportunity to verify that your company meets the criteria for recognition as a Young University Enterprise and to seek the tax authorities’ opinion. This process therefore allows you to receive official confirmation of your eligibility for JEU status.

To obtain a JEU ruling, you must submit a request to the tax authorities. This request must be made in writing, typically in the formof a registered letter with return receipt requested. The tax authorities then have three months to respond.

If the response is favorable, you will be able to take advantage of the tax and social security benefits associated with JEU status. Furthermore, if no response is received by the specified deadline, approval is deemed to have been granted.

The JEU ruling therefore provides you with certainty regarding your eligibility for JEU status, which can be helpful in planning your activities and taking advantage of the associated tax and social security benefits.

Compatibility with other diets

The University Student Enterprise (JEU) program may be compatible with other tax incentives, thereby offering additional opportunities to eligible companies.

Research Tax Credit (CIR)

The JEU is eligible for the Research Tax Credit (CIR), which encourages research and development activities by companies. Eligible research expenses incurred by a JEU may be included in the calculation of the CIR, provided they meet the specific criteria defined by tax law.

Innovation Tax Credit (CII)

The Innovation Tax Credit (CII) is intended to promote innovation activities prior to a product’s market launch. It can also be combined with the JEU or CIR.

Other devices

In addition to the schemes mentioned above, the JEU may be compatible with other tax and regulatory measures, such as government grants, European funding, or public-private partnerships. Compatibility will depend on the specific terms of each measure and the company’s particular circumstances.

Dynergie, a consulting firm, can help you obtain your JEU status

Dynergie will guide you through the process of obtaining and maintaining your JEU status. You can view our services on the following page.

Useful links:

Related articles

Damien Villiers-Moriamé

I assist innovative companies of all sizes in securing public funding (CIR-CII, JEI, bpifrance, CIN, etc.). My technical expertise spans a variety of fields, including IoT, AI, e-learning, embedded systems, and service robotics. My daily work involves supporting entrepreneurs through key and critical stages of their projects (developing a financing plan, creating a business plan, and validating the business model).